| Home | Main Menu |

|

|

ATM 'Conversion Fees'

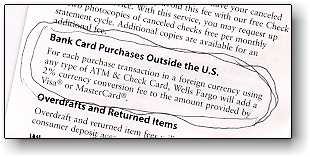

ABOVE: Wells Fargo slipped this bombshell into a statement insert a few years ago, when the trend toward "conversion fees" began.

Most experienced travelers will tell you that ATMs are the cheapest way to get cash overseas. For that matter, so does Visa, which handles currency conversion for banks around the world. Here's a statement from the Visa Global ATM Network Web page:

Well, think again. Most banks tack an additional "conversion fee" onto the Visa or MasterCard currency-exchange commission. Not only that, but this hidden surcharge is on top of the flat "ATM-use" or transaction fees that banks often charge for ATM withdrawals away from home. Example: Wells Fargo, one of the largest banks in the U.S., charges a conversion fee "for each purchase transaction in a foreign currency using any type of ATM & Check Card." The charge, which was recently raised from 2% to 3%, is in addition to the standard 1% currency-exchange commission levied by the Visa/MasterCard international clearinghouse. Let's do the math: For a withdrawal of US $100 in a foreign currency, a Wells Fargo customer is paying a $1 currency-exchange commission to the international clearinghouse, an additional $3 Wells Fargo conversion fee or surcharge, plus a flat $5 ATM transaction fee. Total cost: $9, which is equal to an eye-popping 8% exchange commission. Such fees aren't limited to banks in the U.S. Many British banks now have "currency conversion fees," and the epidemic has spread to other countries. In June, 2007, an Australian reader reported:

How can you avoid being gouged by high ATM surcharges?

Bottom line: As banks lose income from traveler's checks, they're looking for new ways to extract money from overseas travelers. Check your bank's policy on conversion and transaction fees before you use an ATM card abroad--and if you feel that your bank's fees are unreasonable, look for a less greedy bank.

About the author:

After 4-1/2 years of covering European travel topics for About.com, Durant and Cheryl Imboden co-founded Europe for Visitors in 2001. The site has earned "Best of the Web" honors from Forbes and The Washington Post. For more information, see About Europe for Visitors, press clippings, and reader testimonials. |

|

|

| Europe for Visitors - Home | | About us | | Press clippings | | Testimonials | Disclosure: Where hotel or other reservation links point to third-party booking sites, we may receive a small commission on transactions. This will not affect the rate you pay. Copyright © 1996-2026 Durant and Cheryl Imboden. All rights reserved. |